ECONOMYNEXT – Sri Lanka’s rupee has depreciated despite a current account surplus and reserve accumulation has slowed, amid large debt repayments, World Bank Country Economist for Sri Lanka Shruti Lakhtakia said.

Depreciation Despite Current Account Surplus

“Despite the current account surplus and the net purchase of foreign exchange by the

central bank, the reserve accumulation has slowed and the rupee has depreciated so far in 2025,” she told reporters in Colombo after the release of a Sri Lanka Development Update.

There have been claims made in countries with policy rates and no clean float, that external troubles come from current account deficits and not the flawed operating framework of a central bank, analysts have pointed out.

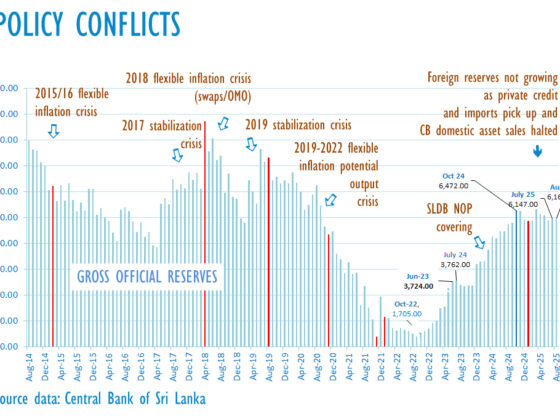

The central bank continued to purchase foreign exchange totaling 1.2 billion dollars up to August 2025, at a slower pace (38.8 percent reduction, y-o-y) compared to the first eight months of 2024, the report said.

As a result, gross usable reserves (excluding the swap with the People’s Bank of China) were

at 4.8 billion dollars by end-August 2025, similar to levels prevailing at end-2024.

However, reserves in terms of import cover fell to 2.5 months in July 2025, lower than 3 months at end-2024.

The net foreign assets of the overall banking system, which turned positive in May 2024, broadly strengthened and then began to decline since April 2025, reaching 2.9 billion dollars in July 2025.

Huge Debt Repayments

But the government’s external debt servicing needs were high, at 1.4 billion dollars in the first half of 2025 alone, the report said.

“So it has slowed down, like we said, and this is because the government is making huge debt service payments,” Lakhtakia said.

“We expect the reserve accumulation to pick up again next year once some of the key swap lines, for example, the ACU swap is amortized and that should be done by next year. So with that, hopefully reserve accumulation will pick up again.

“But it is something we are watching very closely. It is also linked to monetary policy in terms of the interest rates and the global environment.”

In Sri Lanka, a narrative had been floated that debt repayments would begin in 2028, which is widely believed.

Analysts had warned at the beginning of the latest IMF program that a note-issue bank cannot ‘cut’ rates claiming past statistical inflation was low, where it had obligations to collect reserves and apparently also to provide dollars to the Treasury to repay debt against its notes.

Any attempts to ‘cut’ rates by expanding reserve money (its note-issue) will lead to forex shortages and a currency crisis as happened in 2012, 2015 and 2018, eventually leading to failed IMF programs with missed reserve targets given the experience in 2018.

RELATED : Sri Lanka interest rates are dictated by the IMF reserve target, not inflation

This time however the net international reserve target may be met, analysts say as dollars continue to be collected without forex shortages being triggered, with inflationary open market operations apparently stopped at least for the moment.

Gross reserves are down in part due to the central bank settling Reserve Bank of India and IMF loans taken for an earlier crisis from rate cuts, which however tends to improve net reserves.

Domestic Assets of the Central Bank

Analysts have blamed the slowdown in reserve collections on the lack of requirement to reduce domestic assets of the central bank in the current IMF program.

A sell-down of central bank domestic assets to banks lead to a sterilized purchase of dollars, where the liquidity generated from the dollar purchase cannot be used by the banking system to expand credit either to private creditors (for imports) or the government (for debt repayment).

A sell-down of domestic assets therefore leads to an automatic correction in market interest rates sufficient to collect the reserves, by curbing domestic credit, even momentarily.

At the moment such permanent reserve collections are limited to coupon repayments on the central bank’s bond stock and any expansions in demand for its notes (reserve money minus excess liquidity) by the public.

In August and September, the central bank bought more dollars than in earlier months. (Colombo/Oct08/2025)