After the financial and real estate crisis that began in 2008, in 2012 the Government then chaired by Mariano Rajoy created the Asset Management Company from Bank Restructuring (Sareb)better known as “bad bank”.

He did it within the rescue the Spanish banks, which was borne by all taxpayers through a debt guaranteed by the State of more than 50,000 million euros.

The objective was to recapitalize those financial entities affected by the crisis, cleaning up their bank balance sheets after the real estate bubble burst. Sareb bought the toxic real estate assets of the rescued entities for a value of 50,781 million eurosfinancing it with the issuance of debt guaranteed by the State.

It was intended that it would sell those assets – homes and land – that the banks could not recover after the outbreak of the brick crisis, generating capital gains, in order to later be able to return the debt subscribed.

At that time, the Minister of Economy, Luis de Guindos, even stated that the management of such assets by Sareb would offer a return of 15% throughout their life, estimating a period of about 15 years to achieve that objective. He also claimed that It would not cost taxpayers, although it admitted that there could be losses in the first years.

In practice, thirteen years later, Sareb has recorded losses since the beginning and it is currently considered that it will not meet its profitability forecasts. Valuation of toxic assets was too optimisticin view of the price reductions that such assets have been suffering.

Management has not been efficient either, mainly due to the difficulty of disposing of this type of assets (unsold portfolio and unpaid debt). According to the latest available data, from the end of 2024, the portfolio of toxic assets has been reduced by 63.6% to reach 18,999 million euros in assets still pending to be sold, of which 12,050 million are real estate and 6,949 million are failed developer loans.

At the same time, Sareb’s own litigation and management expenses have been multiplying, with more than 200 employees and additional expenses from “service” providers – investment fund companies such as KKR or Blackstone – to which the essential activity is outsourced, that is, help with transactions.

The result is that, in these three decades, the real accumulated profitability of Sareb is clearly negative, around -10%, reflecting sustained losses. Initially, between 2013-2016, with recurring losses due to the drastic drop in the value of real estate assets. Later, between 2017–2019, it saw a slight improvement in sales, but without significant net profits.

Subsequently, the impact of the pandemic aggravated the situation and Sareb accumulated losses of more than 10,000 million euros in 2021.

In 2022, when it became clear that the expected profitability would not be achieved, the State assumed control of Sareb, which became more than 50% public. To continue with the liquidation of assets, but with a residual value much lower than expected.

And to change its mission, so that the homes and land that contributed to the rescue of the financial entities could be transferred to the new public housing company Sepes and serve the general interest: constitute a public housing stock for rent.

At the beginning of this year, more than 40,000 homes and nearly 2,400 plots with the capacity to house around 55,000 homes were transferred free of charge.

Welcome to the social turn of Sareb, a company that did not fulfill its initial objective of recovering the financial rescue through the sale of toxic assets, but that will at least contribute to the objective of have a public housing stock for affordable rental so necessary in our country.

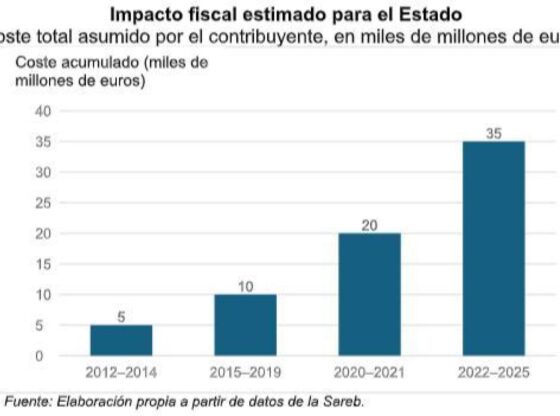

After thirteen years, what was suspected is confirmed: Sareb has been a burden on public accounts, with accumulated losses and a significant fiscal impact. For now, The total cost for the taxpayer is estimated at more than 35,000 million euros.

In 2027, Sareb will go into dissolution and its liquidation will mean a new bill for taxpayers. On the one hand, at that time the Treasury will have to pay the bondholders the difference between what Sareb borrowed to buy the assets and what it actually manages to collect from the sales, since the real market value is clearly lower than what was paid to the rescued savings banks – currently the figure of this negative equity is around 16,464 million euros.

Besides, Sareb will continue to operate until its liquidation year 2027, predictably accumulating new losses and without being able to sell or transfer all real estate and financial assets to third parties – according to the sector, it is estimated that around 6,000 million euros – and the State will finally have to assume them. Possibly an organization like SEPI will have to sell them helped, once again, by servicers.

In short, the bad bank was a bad invention, as one could imagine. Instead of the promised 15% returns, it has generated recurring losses borne by taxpayers. Losses were inevitable.

Aware of the housing problem in our country, and the need to increase supply, at least Sareb has been able to redirect itself to provide the State with a housing stock that can be used for affordable rentals. It’s a shame that this social shift did not occur much earlier.

*** Mónica Melle Hernández is a professor of Economics at the UCM.